Beauty Unlocked

Where Has All The Volatility Gone?

Jun

For a while, the stock market has had the emotional range of a houseplant. Headlines shout about inflation, elections, AI disruption, geopolitical tension, government debt, and consumers doing financial gymnastics at the grocery storeyet broad market volatility often refuses to act impressed. The S&P 500 keeps absorbing shocks, the VIX drifts back toward calm, and investors start asking the same question: where has all the volatility gone?

The answer is not that risk vanished. Risk never retires. It just changes clothes, grows a mustache, and hides in a different part of the market. Volatility may look quiet at the index level, but underneath the surface, single stocks, sectors, options markets, currencies, bonds, and commodities can still be throwing a small furniture-breaking party.

This article explains why market volatility can disappear from the headlines, why the VIX can look calm while investors are still nervous, and what low volatility means for portfolios. Spoiler: calm markets are not always safe markets. Sometimes they are simply markets holding their breath.

What Does “Volatility” Actually Mean?

In investing, volatility describes how much prices move over time. If a stock moves up and down dramatically, it is volatile. If it gently climbs like it has a yoga instructor whispering affirmations in its ear, volatility is low.

There are two major types of volatility investors discuss:

Realized Volatility

Realized volatility is what already happened. It looks backward at actual price movement. If the S&P 500 moved only a little each day over the past month, realized volatility would be low.

Implied Volatility

Implied volatility looks forward. It is derived from options prices and reflects how much movement traders expect in the future. The famous Cboe Volatility Index, better known as the VIX, measures expected 30-day volatility in the S&P 500 based on options prices.

The VIX is often called Wall Street’s “fear gauge,” which sounds dramatic enough to deserve its own movie trailer. When investors aggressively buy protection against market drops, implied volatility tends to rise. When they feel calmor at least calm enough not to pay up for protectionthe VIX often falls.

Why Has Market Volatility Been So Low?

Low stock market volatility usually does not have one single cause. It is more like soup: several ingredients simmering together until the market tastes suspiciously calm.

1. Investors Have Become Used to Bad News

Markets are not moved only by good or bad events. They are moved by surprises. If investors already expect inflation worries, Federal Reserve uncertainty, political noise, and occasional geopolitical stress, those issues may not shock prices the way they once did.

Think of it like living next to a train track. At first, every train rattles your bones. After a while, you can sleep through it. Markets can become similarly numb when the same risks keep showing up wearing the same hat.

2. Corporate Earnings Have Helped Cushion the Market

Strong corporate earnings can suppress volatility because they give investors a reason to keep buying dips. When companies continue to grow profits, raise guidance, or talk confidently about future demand, the market becomes harder to scare.

In recent years, enthusiasm around artificial intelligence, cloud computing, automation, semiconductors, and productivity gains has supported large-cap stocks. That does not mean valuations are risk-free, but it helps explain why scary headlines have not always turned into scary index declines.

3. Passive Investing Smooths Some Market Reactions

The rise of index funds and exchange-traded funds has changed market behavior. Automatic contributions to retirement accounts, target-date funds, and passive index products can create steady demand for equities. This “set it and forget it” flow may reduce panic selling during routine pullbacks.

Of course, passive investing does not eliminate volatility. If everyone rushes for the exits at once, the exits are still the same size. But steady inflows can make everyday market declines feel less dramatic.

4. Options Trading Has Changed the Volatility Landscape

One of the biggest changes in modern markets is the explosion of short-dated options, especially zero-days-to-expiration options, or 0DTE options. These contracts expire the same day they are traded and allow traders to bet on very short-term moves.

This has created a strange market environment. On one hand, heavy options activity can increase intraday movement. On the other hand, dealers hedging options exposure may sometimes dampen larger index swings, depending on positioning. The result can be a market that feels jumpy minute to minute but strangely calm by the closing bell.

5. Volatility Has Moved Beneath the Index Surface

The S&P 500 can look calm even when individual stocks are acting like caffeinated squirrels. This happens when gains in some mega-cap names offset weakness elsewhere. The index barely moves, but under the hood, sectors may be rotating aggressively.

For example, technology stocks might surge while utilities sag, or banks might rally while consumer stocks stumble. The broad index says, “Nothing to see here.” Your individual holdings say, “Excuse me, I am seeing plenty.”

Low VIX Does Not Mean Low Risk

A low VIX can suggest that investors expect smaller near-term moves in the S&P 500. But it does not mean the market is safe, cheap, or immune to shocks. The VIX is not a crystal ball. It is more like a weather forecast: useful, imperfect, and occasionally embarrassed by reality.

Low volatility can even create its own danger. When markets stay calm for too long, investors may begin taking more risk. They may increase leverage, chase momentum, sell options for income, ignore hedges, or assume every dip will be bought. That is when markets become vulnerable to sudden air pockets.

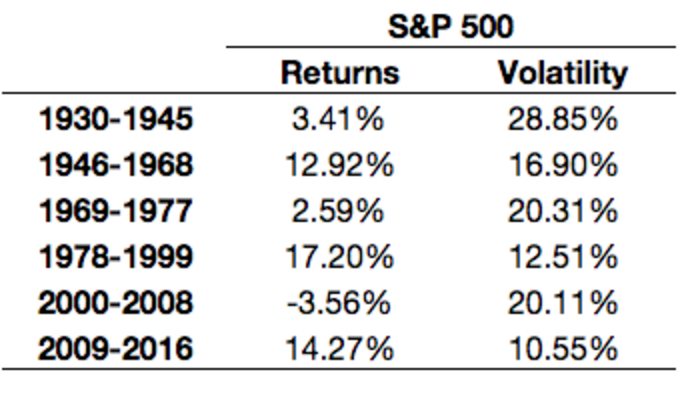

History has repeatedly shown that volatility often returns quickly. Calm markets tend to drift. Volatile markets tend to teleport.

Where Did Volatility Go? It May Be Hiding in These Places

Single Stocks

Index volatility can be low while single-stock volatility remains high. Earnings reports, AI spending concerns, regulatory changes, lawsuits, product launches, and analyst downgrades can all cause large moves in individual companies.

Bonds

Interest-rate volatility has become a major driver of investor anxiety. Treasury yields influence mortgage rates, corporate borrowing costs, equity valuations, and the discount rate used to price future earnings. When bond yields move sharply, stocks may eventually pay attentioneven if they pretend not to at first.

Commodities

Oil, natural gas, gold, and agricultural commodities can react quickly to supply shocks, weather, wars, tariffs, and currency moves. Commodity volatility may not immediately show up in the VIX, but it can affect inflation expectations and corporate margins.

Currency Markets

A stronger or weaker U.S. dollar can impact multinational earnings, emerging markets, commodities, and global trade. Currency volatility often sits outside the average investor’s daily radar, but it can quietly shape market conditions.

Private Markets

Not all volatility is visible every day. Private equity, venture capital, commercial real estate, and private credit do not mark prices as frequently as public stocks. That can make them appear smoother than they really are. Sometimes volatility is not goneit is simply not being priced every second.

Why Calm Markets Can Feel So Strange

Investors are emotionally trained to expect market chaos when the world feels chaotic. So when headlines are loud but volatility is low, it creates cognitive dissonance. Your news feed says “danger.” Your portfolio says “meh.” Your brain says, “One of you is lying.”

The explanation is that markets are discounting machines. They care less about whether conditions are perfect and more about whether conditions are better or worse than expected. If investors expected disaster and received “fine, with some weird spots,” stocks can rise and volatility can fall.

Also, modern markets are extremely liquid, fast, and data-driven. Information is absorbed quickly. Shocks that once took days to process may now be priced within minutes. This can make volatility spikes shorter, even when the underlying risks remain real.

What Low Volatility Means for Investors

Do Not Confuse Calm With Certainty

Low volatility is not a permission slip to abandon risk management. It simply means markets have recently been less jumpy or expect fewer near-term jumps. That can change quickly after an inflation surprise, earnings disappointment, central bank shift, geopolitical event, or credit scare.

Rebalance Before the Storm, Not During It

The best time to review risk exposure is when markets are calm. Waiting until volatility spikes is like shopping for an umbrella during a hurricane. Technically possible, but not ideal.

Investors should check whether their stock allocation, bond duration, cash reserves, and sector exposure still match their goals. A portfolio that felt sensible two years ago may now be more concentrated than expected, especially if a few large technology stocks did most of the heavy lifting.

Keep Cash Useful, Not Emotional

Cash can reduce portfolio volatility and provide flexibility during market selloffs. But holding too much cash out of fear can create opportunity cost. The key is to define the purpose of cash: emergency needs, near-term spending, or dry powder for future investments.

Understand What You Own

Low index volatility can hide concentration risk. Many investors believe they own “the market” but may actually own a portfolio heavily influenced by mega-cap technology and growth stocks. That is not automatically bad, but it should be intentional.

Could Volatility Come Back?

Absolutely. Volatility is like glitter: once released, it gets everywhere.

Possible catalysts include a surprise change in Federal Reserve policy, inflation reacceleration, a sharp rise in bond yields, weakening consumer spending, credit-market stress, geopolitical escalation, disappointing AI returns on investment, or a major earnings reset from market leaders.

The important point is not to predict the exact trigger. Investors have a terrible habit of preparing for the last crisis while the next one sneaks in through a side door. Instead, build a portfolio that can survive multiple types of unpleasant surprises.

How to Navigate a Low-Volatility Market

1. Avoid Chasing Performance Blindly

When volatility is low and markets grind higher, it is tempting to pile into whatever has been working. That strategy feels brilliant until momentum reverses. Strong trends can continue, but late entries require discipline.

2. Diversify Across Real Risk Factors

Diversification is not owning twelve funds that all hold the same seven stocks. Real diversification means spreading exposure across asset classes, sectors, geographies, market capitalizations, and investment styles.

3. Consider Quality

Companies with strong balance sheets, durable cash flows, pricing power, and reasonable debt levels may hold up better when volatility returns. Quality does not prevent losses, but it can reduce the odds of owning businesses that need perfect conditions to survive.

4. Do Not Sell Protection Too Casually

Option-selling strategies can look attractive when volatility is low, but they carry risks. Picking up small premiums can feel easy until one sharp market move wipes out months of income. There is no free lunch in financeonly lunches with footnotes.

5. Create a Volatility Plan

Before the next selloff, decide what you will do if the market drops 5%, 10%, or 20%. Will you rebalance? Buy gradually? Hold steady? Raise cash? A written plan helps prevent emotional decision-making when markets get loud.

Practical Experiences: What Low Volatility Feels Like in Real Life

The oddest part of a low-volatility market is not the calm itself. It is how quickly investors adapt to it. After enough quiet weeks, a 1% down day starts to feel personally offensive. People refresh their brokerage apps and say, “Is this allowed?” Yes, unfortunately. Stocks still move.

Many investors experience low volatility as a slow confidence drip. At first, they are cautious. Then the market keeps rising. Then dips get bought. Then scary headlines fail to matter. Eventually, caution starts to feel silly. This is usually when risk sneaks into portfoliosnot through one dramatic decision, but through small choices that seem harmless at the time.

Someone increases their equity allocation “just a little.” Someone else buys a concentrated thematic ETF because artificial intelligence is “obviously the future.” Another investor sells covered calls, then sells more, then wonders why the strategy feels like collecting pennies in front of a very polite steamroller. Low volatility makes risk feel theoretical. High volatility sends the invoice.

Another common experience is frustration. Conservative investors may feel left behind when markets rise calmly without giving them a dramatic entry point. They wait for a pullback. The pullback does not come. Then they finally buy after a big rally, just in time for normal volatility to return and make them question every life choice since high school.

Long-term investors can learn a useful lesson here: calm markets reward preparation, not prediction. If your plan depends on perfectly timing volatility, the plan may need a nap and a glass of water. A better approach is to invest according to goals, time horizon, and risk tolerance, then rebalance when markets drift too far from target allocations.

Business owners and executives also feel low volatility differently. A calm stock market can improve confidence, reduce financing anxiety, and support dealmaking. But it can also encourage aggressive assumptions. Companies may borrow too much, expand too quickly, or assume capital will remain cheap and available. When volatility returns, the businesses that prepared for tougher conditions often look boring in the best possible way.

For everyday savers, the experience is simpler: low volatility is pleasant, but it should not become a sedative. Retirement accounts look stable. Monthly contributions buy shares without drama. Financial media has to work harder to sound urgent. That is good. But it is still wise to check emergency funds, debt levels, insurance coverage, and portfolio concentration before markets become exciting again.

The best investors do not treat low volatility as proof that nothing can go wrong. They treat it as a chance to tidy the garage before the storm. They review positions, trim excess risk, automate contributions, harvest losses when available, and make sure their portfolio is not secretly one giant bet wearing a fake mustache.

Conclusion: Volatility Is Not GoneIt Is Waiting

So, where has all the volatility gone? It has not disappeared. It has rotated beneath the surface, shifted into single stocks, appeared in short-dated options, moved through bonds and commodities, and occasionally hidden behind strong index performance.

Low volatility can be a sign of confidence, liquidity, strong earnings, and stable expectations. It can also be a sign of complacency. The challenge is knowing that both can be true at the same time.

Investors do not need to fear calm markets. Calm is useful. Calm allows planning, rebalancing, and rational decision-making. But investors should respect calm markets because they can change quickly. Volatility often returns when portfolios are least prepared and when everyone has decided risk is old news.

The smartest response is not panic. It is preparation. Build a portfolio that can handle surprise, avoid overconfidence, understand your exposures, and remember that the market’s quiet voice can still say very important things.

Note: This article is for educational and editorial purposes only. It is not personal financial advice, investment advice, or a recommendation to buy or sell any security.