Beauty Unlocked

Are Small and Mid Cap Stocks Getting Pricey?

May

Small and mid cap stocks are back in the market conversation, which is usually what happens after investors spend a long time ignoring them and then suddenly remember that the stock market has more than seven famous technology companies. The big question now is simple: are small and mid cap stocks getting pricey, or are they still sitting in the bargain bin with a slightly wrinkled price tag?

The honest answer is: it depends on which part of the market you are looking at, which valuation measure you use, and whether earnings actually show up on time. Small cap and mid cap stocks are not one neat basket. Some are profitable, cash-rich, and quietly growing. Others are heavily indebted, rate-sensitive, and one weak quarter away from needing a motivational poster in the finance department.

At a broad level, U.S. small and mid cap valuations do not look wildly expensive compared with large caps. In fact, many valuation measures still show mid caps trading at meaningful discounts to the S&P 500, while quality-screened small caps look more reasonable than the headline Russell 2000 sometimes suggests. But that does not mean the entire small and mid cap universe is cheap. After a strong rebound, the easy-money phase is probably over. Investors now need to separate “undervalued” from “cheap for a reason.”

What Counts as Small Cap and Mid Cap?

Small cap stocks generally refer to companies with smaller market capitalizations, often roughly between $300 million and $2 billion, though definitions vary by index provider and fund. Mid cap stocks usually sit between small caps and large caps, often in the range of about $2 billion to $10 billion or more. In real life, these categories are less like strict school grades and more like airport boarding groups: useful, but not always perfectly organized.

The most common benchmarks include the Russell 2000 for small caps, the S&P SmallCap 600 for quality-screened small caps, and the S&P MidCap 400 for mid-sized companies. The difference matters. The S&P SmallCap 600 requires companies to meet liquidity and financial viability standards, which can make it a higher-quality small cap benchmark than indexes that include more unprofitable firms.

This is why two people can argue about small cap valuations and both sound correct. One may be looking at the Russell 2000, where a large share of companies can be unprofitable. Another may be looking at the S&P 600, where profitability screens make the valuation picture cleaner. Same neighborhood, different houses.

So, Are Small and Mid Cap Stocks Expensive?

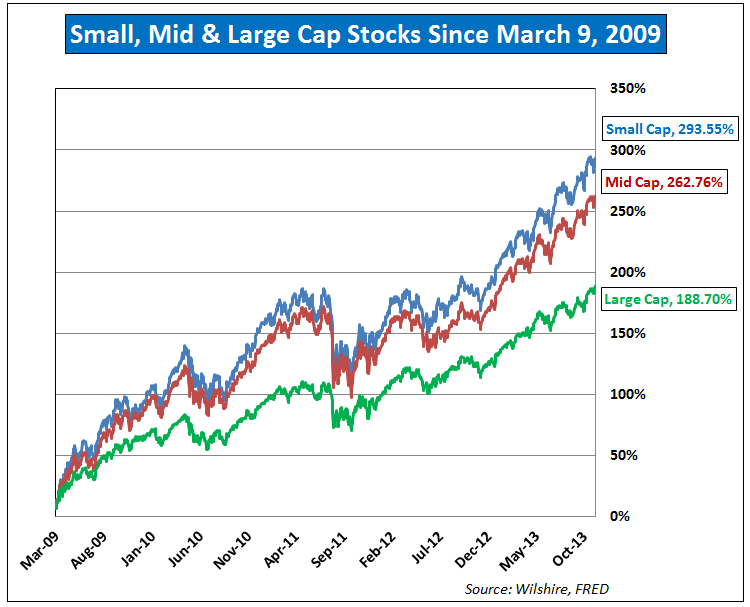

Compared with large caps, many small and mid cap stocks still appear reasonably valued. The S&P 500 has been trading at elevated forward price-to-earnings levels, supported by strong earnings from mega-cap technology, artificial intelligence leaders, and large global businesses. Meanwhile, mid caps have generally traded at lower forward P/E ratios, and the S&P MidCap 400 has recently been around the mid-to-high teens on forward earnings estimates.

Small caps are trickier. The S&P SmallCap 600 forward P/E has recently been near the mid-teens, which does not scream “bubble.” But the broader Russell 2000 can look more expensive because unprofitable companies distort the earnings base. In other words, small caps are not automatically cheap just because they are small. A small company with no earnings is not a bargain; it is a story stock wearing a tiny hat.

The Relative Valuation Argument

The strongest bullish argument for small and mid cap stocks is relative valuation. Large cap indexes, especially the S&P 500, have become highly concentrated in a small group of mega-cap companies. Those leaders may be excellent businesses, but excellence already has a cover charge. When investors pay high multiples for predictable growth, future returns depend heavily on those companies continuing to deliver.

Mid caps, by contrast, often offer a mix of established business models and faster growth potential than mature large caps. Many mid-sized companies are past the fragile startup stage but still have room to expand markets, improve margins, acquire competitors, and attract institutional attention. That middle-child status can be annoying at family dinners, but useful in a portfolio.

Small caps offer a different appeal. They are more domestically focused, less covered by Wall Street analysts, and more likely to benefit if economic growth broadens beyond the biggest companies. The catch is that small caps are also more exposed to financing costs, wage pressure, and economic slowdowns. A cheap valuation can quickly become a value trap if earnings estimates keep falling.

Why Valuation Alone Does Not Tell the Whole Story

Valuation is important, but it is not magic. A stock trading at 14 times earnings can be expensive if profits are about to collapse. A stock trading at 25 times earnings can be reasonable if profits are growing quickly and reliably. Price matters, but so does the “E” in P/E. Investors sometimes forget that earnings estimates are not stone tablets; they are educated guesses with spreadsheets.

For small and mid cap stocks, earnings quality is especially important. Smaller companies often have less pricing power, narrower profit margins, and weaker access to capital markets. J.P. Morgan market data has shown that small caps have had lower interest coverage ratios and a much higher percentage of unprofitable companies than large caps. That matters in a world where interest rates remain well above the ultra-low levels investors enjoyed after the global financial crisis and during the pandemic era.

When borrowing costs are high, small companies feel it faster. Many use floating-rate debt or need refinancing more often than large companies. A mega-cap firm can issue bonds at attractive rates and receive investor applause. A small firm tries the same thing and may get a polite cough from the bond market.

The Interest Rate Factor: The Market’s Gravity

Interest rates are one of the biggest reasons small and mid cap stocks have struggled to sustain leadership. The Federal Reserve’s target range remains far higher than it was during the easy-money years, and Treasury yields have stayed elevated. Higher yields make future earnings less valuable, raise borrowing costs, and give investors more competition from bonds and cash.

This matters because small and mid cap companies tend to be more sensitive to credit conditions. If rates fall meaningfully, small caps could get a tailwind from lower interest expense and improved investor risk appetite. If rates stay high or rise further, weaker balance sheets may remain under pressure. That is why the small cap trade is often also a rate-cut trade, even when investors do not say it out loud.

Mid caps may be better positioned than small caps in this environment. Many mid cap companies have stronger balance sheets, more stable profits, and better access to financing. They are not immune to higher rates, but they usually have more tools than smaller firms. This is one reason some investors see mid caps as the “Goldilocks” segment: not too huge, not too fragile, and sometimes priced more sensibly than either extreme.

Market Breadth: A Key Clue for Small and Mid Caps

Another major theme is market breadth. For much of the recent bull market, large cap technology and AI-related stocks carried the indexes. That narrow leadership made small and mid caps look forgotten. But when market gains begin to spread beyond mega-cap technology, smaller companies often get a second look.

BlackRock’s recent equity outlook has highlighted signs of U.S. market broadening, even while noting that concentration remains high. That is important because small and mid cap stocks usually need broader participation to outperform. They do not benefit as much when investors pile into only a handful of giant companies. They do better when the market begins rewarding industrials, financials, health care, consumer discretionary, energy, and other economically sensitive sectors.

If earnings growth broadens in 2026 and beyond, small and mid cap valuations may prove reasonable. If growth remains concentrated in mega-cap tech, smaller stocks could continue to look cheap without acting cheap. Investors know this painful pattern well: the stock looks undervalued, stays undervalued, then sends a holiday card from the same undervalued address three years later.

Small Caps: Cheap, Risky, or Both?

Small cap stocks may still offer opportunity, but the group is uneven. The S&P SmallCap 600 looks more attractive than the broader small cap universe because it screens for financial viability. That does not eliminate risk, but it reduces exposure to the weakest companies. In the Russell 2000, the high share of unprofitable firms can make broad valuation metrics less reliable.

For investors, this means quality matters. A small cap company with positive free cash flow, manageable debt, a defensible niche, and improving margins may deserve a higher multiple. A company burning cash while promising “adjusted profitability someday” deserves skepticism and maybe a very strong cup of coffee.

Small cap value stocks may be especially interesting because they often trade at lower multiples and can benefit from economic normalization. Banks, regional financials, industrial suppliers, specialty manufacturers, and selected health care firms can offer real earnings power. However, investors need to watch credit exposure, loan quality, customer concentration, and margin trends.

Mid Caps: The Forgotten Sweet Spot

Mid cap stocks may be the most compelling part of the discussion. Historically, mid caps have offered a strong blend of growth and durability. They are often established enough to survive difficult economic conditions but still small enough to grow faster than large caps. Many are acquisition targets, industry consolidators, or future large caps in training.

Valuation data has shown the S&P MidCap 400 trading at a discount to the S&P 500. State Street has noted that mid caps have recently traded at a sizable forward P/E discount to large caps, even while offering exposure to U.S. growth. That combination can be attractive, especially when investors worry that the largest companies are priced for perfection.

Mid caps also tend to have less extreme exposure to the weakest small cap balance sheets. They may not deliver the explosive upside of the best tiny companies, but they may provide a smoother ride. Think of mid caps as the sensible friend who still knows how to have fun but also brings a phone charger.

Where Stocks May Be Getting Pricey

Not every small or mid cap area is attractive. Some pockets have already become expensive, especially companies tied to popular themes such as AI infrastructure, defense technology, energy transition, specialized software, and speculative biotech. A good story can push valuations far ahead of earnings, particularly when investors are desperate to find “the next big thing.”

Small cap growth stocks can be vulnerable here. If a company is priced on revenue growth but lacks profits, it needs near-perfect execution. Any slowdown can cause the valuation multiple to shrink quickly. That does not mean all small cap growth stocks are bad. It means investors must be careful about paying large cap-style prices for small cap-level uncertainty.

Some mid cap industrial and infrastructure names have also become more expensive after strong performance. Businesses benefiting from reshoring, automation, aerospace demand, data center construction, or government spending may deserve premium valuations, but the market may already be discounting years of good news. When everyone discovers the same “hidden gem,” it is no longer hidden. It is standing on stage with a spotlight and possibly a valuation problem.

How Investors Can Judge Valuation More Wisely

Instead of asking whether all small and mid cap stocks are pricey, a better question is: which companies are priced for realistic outcomes, and which are priced for fairy tales with quarterly earnings calls?

Investors can start with several practical checks. First, compare a company’s current P/E, EV/EBITDA, and price-to-sales ratios with its own history and industry peers. Second, examine earnings revisions. Rising estimates can support a higher valuation, while falling estimates can make a low multiple misleading. Third, review balance sheet strength, especially debt maturity schedules and interest coverage. Fourth, look at free cash flow, not just adjusted earnings.

It is also useful to compare indexes. The S&P SmallCap 600, Russell 2000, S&P MidCap 400, and Russell Midcap Index can show different valuation pictures because they hold different companies. A broad ETF may be convenient, but investors should understand what is inside it. In small caps, index construction is not a tiny detail; it can change the entire risk profile.

Specific Examples of What to Watch

Regional banks are a good example of the opportunity-risk balance. Many trade at modest valuations and could benefit if the yield curve improves, credit losses remain contained, and deposit costs stabilize. But they are also exposed to commercial real estate, loan quality, and regulatory pressure. Cheap may be justified if the balance sheet is weak.

Small industrial companies are another example. A manufacturer tied to reshoring, aerospace, or automation may have strong long-term demand, but investors should check whether margins are expanding or merely being flattered by temporary price increases. A company with recurring aftermarket revenue may deserve a better multiple than a purely cyclical equipment seller.

Health care small caps can be even more complicated. Some medical device and services companies have durable revenue, while early-stage biotech firms may depend on clinical trial outcomes and capital raises. The valuation tools for each are completely different. Using a simple P/E ratio on a company with no earnings is like using a kitchen thermometer to measure the weather. Technically it has numbers, but good luck.

The Verdict: Getting Pricey, but Not Overheated Everywhere

Small and mid cap stocks are not screamingly cheap across the board anymore, but they are not universally pricey either. Mid caps still look reasonably valued relative to large caps, especially if earnings growth broadens. Quality small caps also appear more attractive than headline small cap indexes may suggest. The riskiest areas are speculative growth stocks, highly leveraged companies, and theme-driven names where prices already assume excellent outcomes.

The most balanced view is that small and mid cap stocks are moving from “ignored and discounted” toward “selectively interesting.” That is a healthier setup than a broad bubble, but it requires more homework. Investors cannot simply buy anything small and expect it to bounce. In this environment, balance sheets, earnings durability, cash flow, and valuation discipline matter more than market-cap labels.

For long-term investors, the opportunity may be real. But patience is essential. Small and mid cap leadership often arrives in bursts, not in perfectly scheduled calendar invitations. The best approach is to focus on quality companies with reasonable valuations, improving earnings, and manageable debt. That way, if the market broadens, you own businesses that can participate. If it does not, you are not left holding the most fragile names in the bargain basket.

Experience-Based Perspective: What Market Cycles Teach About Small and Mid Caps

One useful experience from watching market cycles is that small and mid cap stocks often feel least comfortable right before they become interesting. They rarely ring a bell at the bottom. More often, they sit there looking boring, undercovered, and slightly suspicious while investors chase whatever has been working recently. Then, when earnings improve or rates fall, the same neglected stocks suddenly become “undiscovered opportunities,” even though they were sitting in plain sight the whole time.

Another lesson is that valuation discounts can last longer than expected. Just because small caps trade below large caps does not mean they must immediately outperform. A discount can reflect real concerns: weaker balance sheets, slower earnings revisions, lower margins, or tighter credit conditions. Investors who buy only because something looks cheap may spend years learning the difference between undervaluation and impatience.

In practice, the most useful small and mid cap analysis starts with business quality. A mid cap company with consistent free cash flow, low leverage, and a clear competitive advantage may be worth buying even if it is not the cheapest stock on the screen. Meanwhile, a deeply discounted small cap with shrinking revenue and heavy debt may be a trap. The market is not always efficient, but it is not always foolish either.

Portfolio construction also matters. Small and mid caps can be volatile, so position size should reflect risk. A diversified ETF can reduce single-company blowups, while active managers may add value by avoiding weak balance sheets and unprofitable companies. Investors who prefer individual stocks should be ready for wider price swings and less analyst coverage. Sometimes a small cap drops sharply not because the long-term story changed, but because liquidity disappeared for a day. That is not fun, but it is part of the territory.

The final experience-based takeaway is emotional: do not let the word “small” fool you. Small cap investing is not automatically simple, safe, or early. Some small companies are future stars. Others are permanent residents of the “maybe next year” club. Mid caps can offer a more balanced path, but they still require valuation discipline. When prices rise, investors should ask whether earnings power has improved just as much. If the answer is yes, the stock may still be attractive. If the answer is no, the market may be charging filet mignon prices for a microwave burrito.

So, are small and mid cap stocks getting pricey? Some are. Many are not. The real answer lives in the details: earnings quality, debt, margins, industry outlook, and the price paid. For investors willing to do the work, this part of the market still offers opportunity. For investors hoping every small stock will magically become the next giant, the market may be less generous.

Note: This article is for educational and informational purposes only. It is not personalized investment advice. Readers should research carefully or consult a qualified financial professional before making investment decisions.

Conclusion

Small and mid cap stocks are no longer the forgotten corner of the market, but they are not uniformly overpriced. Mid caps still look attractive relative to large caps in many valuation frameworks, while quality small caps may offer better value than broad small cap headlines suggest. The key is selectivity. Investors should focus on companies with durable earnings, healthy balance sheets, reasonable valuations, and clear catalysts. In today’s market, the label “small cap” or “mid cap” is only the starting point. The real question is whether the business can grow into its price without needing heroic assumptions.