Hair Care

4 Economic Charts That Might Surprise You

Jun

The economy is a bit like a group chat: loud, confusing, and somehow everyone is convinced they are reading it correctly. One person sees a strong job market. Another sees grocery prices doing parkour. A third points to record household wealth. A fourth is quietly wondering why the rent has become a personality trait. That is why economic charts matter. They do not make life magically cheaper, but they do help explain why the economy can look healthy on paper while still feeling like a treadmill with the incline stuck on “mountain goat.”

The most surprising economic charts are rarely the flashiest ones. They are the ones that show two things being true at the same time: growth can continue while confidence sinks, inflation can slow while prices stay painfully high, wealth can hit records while savings shrink, and housing can be technically “affordable” by an index while emotionally unaffordable to everyone who has ever opened a mortgage calculator and whispered, “Absolutely not.”

Below are four economic charts that might surprise you, not because they are strange, but because they reveal the gap between the headline economy and the household economy. Think of them as four windows into the same house: one shows the foundation, one shows the heating bill, one shows the locked front door, and one shows the couch cushions being searched for spare change.

Chart 1: The Economy Can Grow While People Still Feel Stressed

The chart idea: Real GDP vs. consumer sentiment

The first surprising chart compares real gross domestic product, the broadest measure of inflation-adjusted economic output, with consumer sentiment. Real GDP still shows an economy that is expanding. In the first quarter of 2026, the U.S. economy grew at a 1.6 percent annual rate in the second estimate, after growing 0.5 percent in the final quarter of 2025. That is not a rocket launch, but it is not a collapse either. The economy is still moving forward.

Yet consumer sentiment tells a much gloomier story. The University of Michigan’s consumer sentiment index remained historically weak in mid-2026, even after improving in June from the previous month. In plain English, the economy was still growing, but many households were not exactly throwing confetti in the cereal aisle.

Why the disconnect? GDP measures the total size and activity of the economy. It includes consumer spending, business investment, government spending, exports, and more. But families do not experience “gross domestic product” at the kitchen table. They experience gas prices, rent, insurance premiums, child care costs, grocery receipts, interest rates, and whether their paycheck makes it to Friday with dignity intact.

This is the first big lesson: economic growth is not the same thing as economic comfort. A country can produce more goods and services while households still feel squeezed. A business can invest in new equipment while a renter cannot save for a down payment. Corporate profits can rise while a family wonders why a basic fast-food order now requires a small committee meeting.

What this chart would show

One line, real GDP, trends upward over time. Another line, consumer sentiment, drops sharply during inflation shocks and periods of uncertainty. The surprise is not that people feel bad during recessions. The surprise is that people can feel bad even when the economy is technically still growing.

For SEO readers looking for the main takeaway: economic charts often show that the U.S. economy is resilient, but household confidence is more sensitive to prices than to abstract growth statistics. In other words, GDP is the doctor saying, “Your vital signs are stable,” while consumers are saying, “Great, but why does this prescription cost $147?”

Chart 2: Inflation Can Slow While Prices Stay High

The chart idea: Annual inflation rate vs. the consumer price index level

This may be the most misunderstood chart in modern economics. When people hear that inflation is “cooling,” they often expect prices to fall. But lower inflation usually means prices are rising more slowly, not that they are going back to where they were. If your rent jumps from $1,500 to $1,800 and then rises to $1,850 the next year, inflation has slowed. Your wallet, however, is not sending thank-you cards.

In May 2026, the Consumer Price Index for All Urban Consumers was up 4.2 percent from a year earlier. Energy prices were a major driver, with the energy category rising far faster than the overall index. Food and services also remained important parts of the household cost puzzle. The headline number is useful, but the lived experience depends on what people buy most often. Families do not buy “the CPI basket.” They buy eggs, electricity, gasoline, rent, car insurance, and the suspiciously smaller bag of chips that somehow costs more.

The chart that surprises people is not just the inflation rate. It is the price level. The CPI index itself shows that the general cost of living has climbed substantially compared with the pre-pandemic period. Even if monthly inflation slows, the total price level does not automatically reset. It is more like climbing a staircase than riding an elevator back down.

That matters because wages and incomes must catch up to a higher cost base. The Census Bureau reported that real median household income was $83,730 in 2024, not statistically different from the 2023 estimate. That means many households were running hard just to stay in roughly the same place after adjusting for inflation. There is a reason “I got a raise, but I do not feel richer” has become the unofficial anthem of the American checkout lane.

What this chart would show

The inflation-rate line rises and falls, sometimes dramatically. The price-level line mostly climbs. The surprise is that inflation can improve while affordability still feels worse, because households pay today’s price level, not last year’s inflation rate.

This is also why inflation psychology is so sticky. People remember old prices. They remember when a normal grocery trip did not feel like adopting a second mortgage. Economists talk about year-over-year changes; consumers remember the old menu board. Both are real, but they answer different questions.

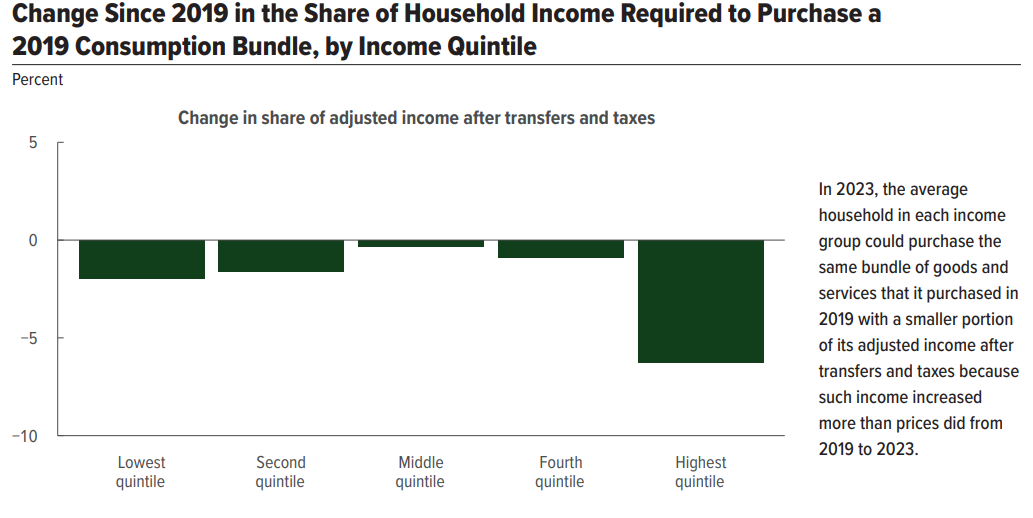

Chart 3: Housing Affordability Is Better Than the Worst Moment, But Still Brutal

The chart idea: Housing affordability index vs. mortgage pressure

Housing is where economic statistics go to lose friends. A housing affordability chart can show some improvement from the worst points of the recent affordability crunch, but still leave buyers staring at listings like they are museum artifacts: beautiful, distant, and not for touching.

The fixed Housing Affordability Index, reported through FRED using National Association of Realtors data, stood at 105.6 in May 2026. In that index, 100 means a family earning the median income has exactly enough income to qualify for a mortgage on a median-priced home, assuming a 20 percent down payment. A reading above 100 sounds comforting, but the details matter. A 20 percent down payment is not a casual footnote. For many first-time buyers, it is the dragon guarding the castle.

The housing chart is surprising because it can look less terrible than it feels. Why? Because “median income,” “median home,” “qualifying income,” and “20 percent down” are clean statistical assumptions. Real life is messier. Buyers have student loans, car payments, child care costs, credit card balances, medical bills, and sometimes a dog with a taste for emergency vet visits. The index may say “possible,” while the household budget says, “Please stop making eye contact with Zillow.”

Higher mortgage rates also change the emotional math. When rates rise, the same home price creates a much larger monthly payment. A buyer who could afford a certain price at 3.5 percent may be locked out at 6.5 percent, even if their income improved. The home did not become nicer. It did not add a secret library or a backyard espresso bar. The financing simply became more expensive.

What this chart would show

A housing affordability line that has recovered somewhat from extreme lows but remains weak by historical comfort standards. The surprise is that affordability can technically improve while homeownership still feels out of reach for younger and first-time buyers.

The housing story also explains why the economy feels different across generations. Homeowners with low fixed-rate mortgages may have large paper gains and stable payments. Renters and would-be buyers face higher rents, high home prices, and expensive borrowing. Same country, different planets.

Chart 4: Household Wealth Is Huge, But Savings Are Thin

The chart idea: Household net worth vs. personal saving rate and debt

The fourth chart is the most “how can both be true?” of the bunch. Household and nonprofit net worth reached roughly $183 trillion in the first quarter of 2026. That is an enormous number. It is so large that it stops sounding like money and starts sounding like something NASA would measure in miles.

At the same time, the personal saving rate fell to 2.6 percent in April 2026. Total household debt reached $18.8 trillion in the first quarter of 2026, according to the New York Fed’s household debt data. Consumer credit continued expanding, and revolving credit, which includes credit cards, remained an important pressure point for many households.

This chart surprises people because “record wealth” and “thin savings” sound contradictory. They are not. Household net worth includes assets such as homes, stocks, retirement accounts, and business equity. Those assets are real, but they are not always liquid. You cannot swipe your home equity at the grocery store. Your 401(k) may be up, but using it to pay the electric bill is not exactly Plan A.

Wealth is also unevenly distributed. A rising stock market can boost aggregate household net worth while doing little for households that own few financial assets. Home equity can enrich longtime homeowners while leaving renters behind. So the national balance sheet can sparkle while many checking accounts look like they just finished a cage fight.

What this chart would show

Household net worth climbs to towering levels, while the personal saving rate sits low and household debt remains elevated. The surprise is that America can look wealthy in the aggregate while many households have limited short-term breathing room.

This is one of the biggest reasons economic headlines can feel out of touch. When analysts say households are wealthy, they may be referring to aggregate assets. When consumers say they are stretched, they may be referring to cash flow. Assets and cash flow are cousins, not twins. One can be healthy while the other is gasping into a paper bag.

Bonus Context: The Federal Budget Chart No One Wants at Brunch

No one likes to bring up federal deficits at a casual meal. It is not exactly sparkling conversation. Still, the budget chart matters because it shapes interest rates, future taxes, public investment, and financial market expectations. The Congressional Budget Office projected that the federal deficit would total $1.9 trillion in fiscal year 2026 and grow to $3.1 trillion by 2036. Debt held by the public was projected to rise from 101 percent of GDP in 2026 to 120 percent in 2036.

The surprising part is not simply that the government borrows money. The surprising part is that net interest costs are becoming a larger driver of the fiscal picture. When interest costs rise, more federal dollars go toward paying for past borrowing instead of current services, infrastructure, research, or tax relief. It is the national version of watching your credit card interest eat the fun money.

This does not mean disaster is guaranteed. The U.S. still has deep capital markets, a powerful economy, and the world’s dominant reserve currency. But the chart is a reminder that higher rates do not only affect homebuyers and businesses. They also affect Uncle Sam, who, like everyone else, discovers that refinancing is less charming when rates are higher.

What These Four Economic Charts Really Tell Us

Taken together, these economic charts reveal a simple but powerful truth: the U.S. economy is not one story. It is a stack of stories. GDP says the economy is still expanding. Inflation data says prices are rising, though the pace changes month to month. Housing data says affordability has improved from the worst readings but remains tight. Household balance-sheet data says wealth is high, yet savings are thin and debt is heavy. Consumer sentiment says people are not grading the economy on a curve.

That is why smart economic analysis needs more than one chart. A single chart can be accurate and still incomplete. GDP without inflation misses the cost-of-living story. Inflation without wages misses purchasing power. Net worth without savings misses liquidity. Housing prices without mortgage rates miss monthly affordability. Consumer sentiment without jobs misses resilience.

For readers, investors, business owners, and everyday budget warriors, the best approach is to ask better questions. Not just “Is the economy good or bad?” but “Good for whom?” “Compared with when?” “Measured by income, wealth, prices, confidence, or cash flow?” That is where the real insight lives.

Experience Section: What These Charts Feel Like in Real Life

If you have ever looked at a strong economic headline and thought, “That is nice, but my bank account did not get the memo,” you have already experienced the lesson of these charts. Economic data can be true at the national level while feeling incomplete at the personal level. A household is not a miniature version of the national economy. It is a living, breathing budget with rent due, groceries needed, insurance renewing, and at least one mysterious subscription hiding in the shadows.

One common experience is the raise that does not feel like a raise. You get a salary increase, celebrate responsibly, and then realize your rent, car insurance, utilities, and grocery bill all quietly formed a coalition against you. On paper, your income rose. In practice, your margin for error stayed the same or even shrank. That is the difference between nominal gains and real purchasing power. It is also why inflation leaves such a long emotional aftertaste. Even when the rate slows, people continue living with the higher price level.

Housing creates another unforgettable experience: the mortgage calculator ambush. You enter a home price that already feels ambitious, add a normal down payment, select a current mortgage rate, and suddenly the monthly payment appears wearing villain music. This is where affordability charts become personal. A small change in interest rates can turn “maybe” into “not unless the basement comes with buried treasure.” Many younger buyers are not just comparing home prices with income. They are comparing monthly payments with every other bill that refuses to leave the party.

Then there is the wealth illusion. Some households may technically be wealthier because their retirement accounts or home values rose. But unless they are selling assets, borrowing against them, or already living comfortably, that wealth may not help with short-term costs. It is possible to have a rising net worth and still feel cash poor. This is especially true for homeowners with valuable houses but tight monthly budgets, or workers whose retirement accounts look better while their checking accounts look like a desert with overdraft protection.

Small business owners feel these charts in a slightly different way. GDP growth may suggest customers are still spending, but inflation changes what they buy and how often they buy it. Higher interest rates make inventory, equipment, and expansion more expensive. Labor market stability is good, but wage pressure and benefit costs can squeeze margins. A restaurant owner, contractor, online seller, or local retailer does not experience “the economy” as one number. They experience supplier invoices, payroll, rent, card processing fees, and whether customers choose the premium option or suddenly become passionate about discounts.

Investors also live inside these charts. Strong household wealth can support spending, but low savings may raise questions about durability. Higher federal interest costs can influence bond markets. Inflation data shapes Federal Reserve expectations. Housing affordability affects builders, banks, furniture stores, moving companies, and local tax bases. The economy is connected like a plate of spaghetti, except the spaghetti occasionally appears on CNBC and argues about interest rates.

The most practical experience is this: economic charts are not fortune-telling devices. They are dashboard lights. One light says growth is still on. Another says inflation pressure remains. Another says housing is tight. Another says households are wealthy but liquidity is uneven. You would not drive by staring at only the speedometer and ignoring the fuel gauge. Likewise, you should not read the economy through one statistic and declare the case closed.

For everyday decision-making, these charts suggest balance. Build cash reserves when possible. Be careful with high-interest debt. Treat homebuying as a monthly-payment decision, not just a home-price decision. Negotiate wages with inflation and local costs in mind. If you invest, remember that aggregate wealth gains do not eliminate risk. And if the economy feels confusing, congratulations: you are paying attention.

Conclusion: The Economy Is Strong, Strange, and Uneven

The four economic charts that might surprise you all point to one conclusion: the economy is not broken in a simple way, and it is not booming in a simple way either. It is strong in some places, strained in others, and deeply uneven across households. Real GDP can expand while consumer confidence weakens. Inflation can slow while prices remain high. Housing affordability can improve slightly while ownership remains difficult. Household wealth can hit impressive levels while savings stay low and debt remains heavy.

That is the real value of economic charts. They help us move beyond slogans. They show why one person can say, “The economy is doing fine,” while another says, “Then why does my grocery receipt look like a ransom note?” Both may be responding to real data, just different parts of it.

So the next time an economic headline sounds too cheerful or too gloomy, look for the chart underneath it. Better yet, look for four. The economy is a movie, not a snapshot, and the plot makes a lot more sense when you stop judging it by a single frame.

SEO Tags

Note: This article synthesizes current U.S. economic data and explains the trends in plain American English for web publication. Data releases may be revised over time.